Welcome:

Login

|

Sign Up

|

About CircleID

Follow:

|

|

|

|

||

|

||

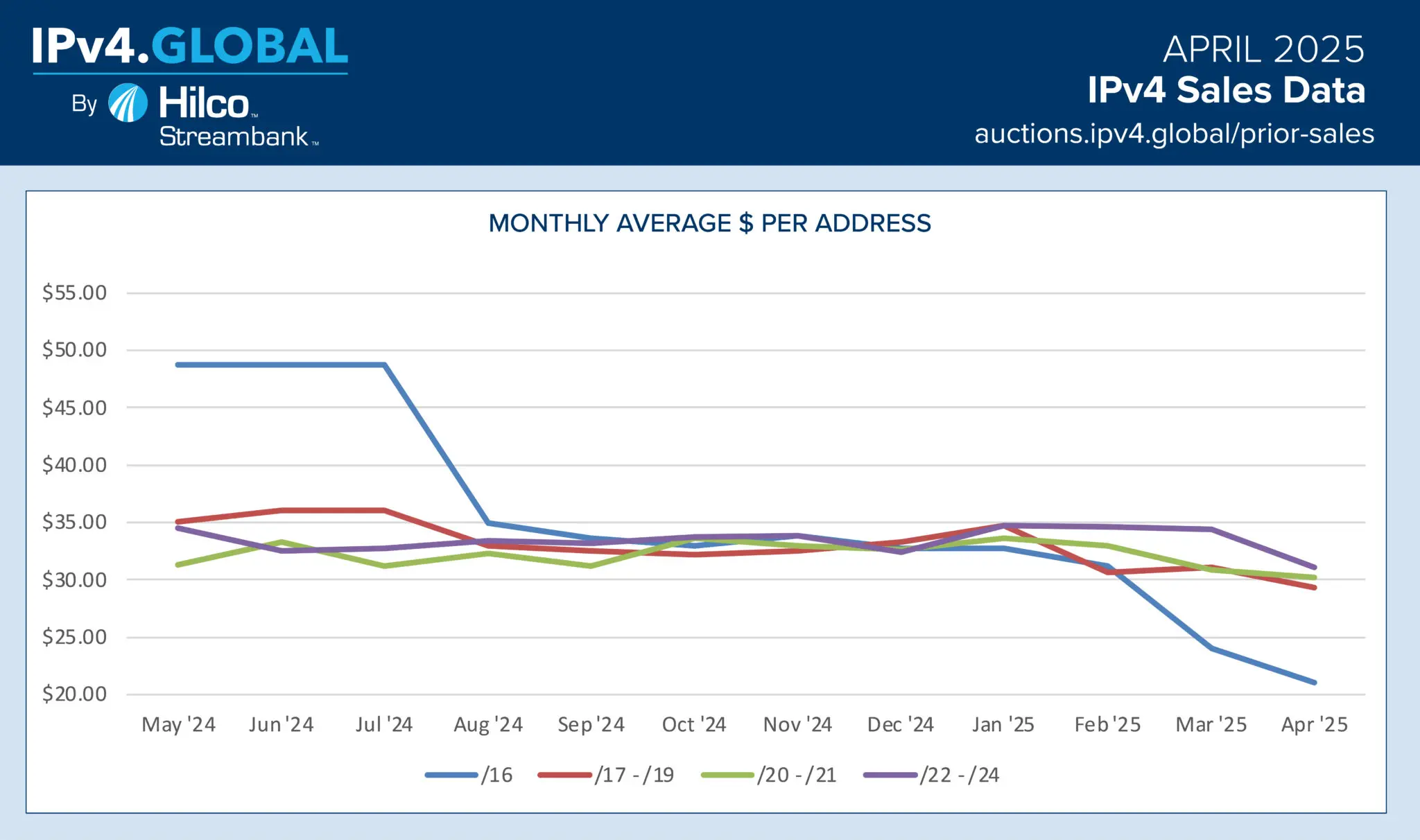

The market for IPv4 addresses is showing signs of a gentle deflation. According to the April 2025 sales data from IPv4.Global by Hilco Streambank, the average price per address has declined across all block sizes. The most notable change comes from /16 blocks—large address groups typically favoured by enterprises—which fell steeply from $50 in mid-2024 to under $30 in April 2025. Smaller blocks such as /22–/24, meanwhile, experienced only modest declines, with average prices holding above $30 until a recent dip in April.

This divergence reflects a growing bifurcation in market dynamics. Large blocks, while commanding premiums due to their administrative convenience, are now facing pricing pressure due to increased supply. As more holders monetize idle assets, particularly in the wake of rising cloud costs and data center consolidation, the influx of available addresses is dragging prices down.

Smaller blocks, often preferred by smaller ISPs and hosting providers, remain more resilient. Their pricing has been buffered by steady demand and limited inventory. Even so, April saw a slight downturn across all categories, suggesting that the overall market may be feeling the weight of oversupply.

Despite declining prices, transaction volume appears stable, indicating continued demand for IPv4 real estate. However, whether this equilibrium holds depends largely on how quickly surplus inventory is absorbed. If supply moderates in the coming months, as sellers exhaust stockpiles, prices may stabilise—though a return to 2022 highs seems unlikely.

For further details on the latest IPv4 transactions, click here and here to track ongoing market trends.

Sponsored byDNIB.com

Sponsored byIPv4.Global

Sponsored byVerisign

Sponsored byWhoisXML API

Sponsored byCSC

Sponsored byVerisign

Sponsored byRadix

A World-Renowned Source for Internet Developments. Serving Since 2002.